Null Hypothesis Significance Test

Once we have a statistical model (or hypothesis), we need to assess whether it's plausible given our data \(\mathcal{D}\).

In this section, we introduce frequentist statistical inference and hypothesis testing. Although

Bayesian inference can replace many frequentist techniques and is especially popular in

modern machine learning, frequentist methods remain valuable tools — they're often simpler to compute, more standardized, and provide

complementary insights.

Here, we discuss the null hypothesis significance test(NHST).

Suppose we have two competing hypotheses:

- Null Hypothesis \(H_0\): This is the default assumption.

- Alternative Hypothesis \(H_1\): This represents the claim we wish to support.

(So, hypothesis testing is a kind of binary classification problem.)

Our goal is to decide which hypothesis is more plausible. Usually, our reasoning is that if \(H_0\) is very unlikely,

then we conclude that \(H_1\) would be true (i.e., we reject the null hypothesis).

Rejecting \(H_0\) does NOT mean \(H_1\) is absolutely true. Conversely, failing to reject \(H_0\) only means

that the evidence is insufficient to support \(H_1\). Thus, our conclusion can be wrong:

- Type I error(or false negative) : Accidentally rejecting the null \(H_0\) when it is true.

- Type II error(or false positive): Accidentally accepting \(H_0\) when the alternative \(H_1\) is true.

The type I error rate \(\alpha\) is called significance of the test. It represents the probability of mistakenly rejecting

\(H_0\) when it is true (typically, set 0.05 to 0.01 in practice.)

To decide whether to reject \(H_0\), we define a function of the data \(\mathcal{D}\) that summarizes the evidence

against \(H_0\). This is called the test statistic, denoted as \(test(\mathcal{D})\).

To evaluate the significance of our observed test statistic, we compare it to what we would expect under the null

hypothesis. That is, we sample the hypothetical dataset \(\tilde{\mathcal{D}}\) assuming \(H_0\) is true and compute

their test statistics, \(test(\tilde{\mathcal{D}})\).

The p-value is defined as the probability, under \(H_0\),

of obtaining a test statistic at least as extreme as the one we observed:

\[

p = P(test(\tilde{\mathcal{D}}) \geq test(\mathcal{D}) | \tilde{\mathcal{D}} \sim H_0).

\]

A "small" p-value (typically, \(< \alpha\)) indicates that the observed result is unlikely under \(H_0\),

leading us to reject the null hypothesis in favor of \(H_1\). Traditionally we reject the null hypothesis

if the p-value is less than \(\alpha = 0.05\), which is called the significance level of the

test. Note that a p-value of 0.05 does NOT mean that the alternative hypothesis \(H_1\) is true with probability

0.95. Indeed, even many scientists misinterpret p-values.

NHST provides a systematic way to evaluate claims, but it has limitations:

- Statistical significance does not imply practical significance. Even if \(H_0\) is rejected, the actual effect size may be too small to be meaningful.

- p-values depend on sample size. With very large datasets, even tiny, practically irrelevant differences may yield small p-values.

- Frequentist methods rely on fixed significance thresholds. Bayesian approaches offer an alternative framework by directly computing the probability of hypotheses given the data.

t-Tests

Example:

Suppose we are analyzing the test scores of students in a school. Historically, the average test score is 70. A researcher

believes that a new teaching method has improved scores. To test this, we collect a sample of 30 students' scores after

using the new method.

- \(H_0\): The new method has no effect, meaning the true mean is still 70.

- \(H_1\): The new method increases the average score, meaning the mean is greater than 70.

We collected a sample of (\(n = 30\)) students with the following observed statistics:

- Sample mean: \(\bar{x} = 75.20\).

- Sample standard deviation \(s = 9.00\)

where

\[

s = \sqrt{\frac{1}{n-1}\sum_{i=1}^n (x_i - \bar{x})^2}.

\]

Since the population standard deviation \(\sigma\) is unknown, we use one-sample t-test.

The test statistic is computed by:

\[

t = \frac{\bar{x} - \mu_0}{s / \sqrt{n}} = \frac{75.20 - 70}{9.00 / \sqrt{30}} \approx 3.16.

\]

The p-value is the probability of observing a test statistic as extreme as (or more extreme than) the calculated

t-value under the null hypothesis. This follows a Student's t-distribution

with \(n -1 = 29 \) degrees of freedom.

Then we have \(p \approx 0.0021\) via some numerical computation. Set the significance level \(\alpha = 0.05\).

Since \(p < 0.05\), we reject \(H_0\). Therefore, there is strong statistical evidence that the new teaching method

increases students' test scores.

We can only say that the data we observed(test scores) are very unlikely under the assumption that the true mean is still 70.

It does NOT mean that..

- the new teaching method definitely increases test scores.

- the probability that \(H_0\) is true is 0.0021.

- the effect is practically significant.

Confidence Intervals vs Credible Intervals

In frequentist statistics, we use the variability induced by the sampling distribution as a way to estimate uncertainty

of a parameter estimate. we define \(100(1 - \alpha)%\) confidence interval(CI). It is common to set the

significance level \(\alpha = 0.05\), which yields a 95% CI. If we repeatedly sampled data, and construct a 95% CI for each data,

then about 95% of such intervals will contain the true parameter \(\theta\).

95% CI does NOT mean that the true parameter lies in the interval with probability 0.95

because, in frequentist statistics, \(\theta\) is treated as a fixed constant.

On the other hand, in Bayesian statistics, we treat the data as fixed (since it is known) and the parameter as random (since

it is unknown). Indeed, the explanation; "the true parameter lies in the interval with probability 0.95." is valid in Bayesian

statistics. Such a interval is called the credible interval.

Example:

Suppose we toss a coin \(n = 100\) times and observe 60 heads. Now we want to estimate the probability of getting heads.

First, we try the frequentist approach. The point estimate for the probability of heads is \(\hat{p} = \frac{60}{100} = 0.6\), and

the standard error(SE) for a proportion is given by:

\[

\begin{align*}

\text{SE} &= \sqrt{\frac{\hat{p}(1-\hat{p})}{n}} \\\\

&= \sqrt{\frac{0.6 \times 0.4}{100}} \\\\\

&\approx 0.049.

\end{align*}

\]

For a 95% CI using normal approximation, the

critical value is \(z_{0.025} \approx 1.96\). Then CI is given by

\[

\begin{align*}

\text{CI} &= [\hat{p}-z_{0.025} \times \text{SE}, \quad \hat{p}+z_{0.025}\times \text{SE}] \\\\

&\approx [0.504, 0.696].

\end{align*}

\]

If we repeated the experiment (tossing the coin 100 times) many times and computed a 95% CI each time, about 95% of those

intervals would contain the true \(p\).

Note: A

z-score is any value that has been standardized to represent the number of standard deviations

away from the mean. The

critical value is a specific z-score used as a threshold in hypothesis testing or

confidence interval calculations. In our case, \(z_{0.025} \approx 1.96\) is the critical value that separates the central

95% of the distribution from the outer 5% (2.5% in each tail).

In Bayesian approach, we assume a uniform prior for the probability \(p\) which is equivalent to

a

Beta distribution:

\[

p \sim \text{Beta}(1, 1).

\]

With 60 heads and 40 tails, the likelihood is given by a binomial distribution. In the Bayesian framework, the

posterior distribution is:

\[

p \sim \text{Beta}(1+60, 1+40) = \text{Beta}(61, 41).

\]

(Note:The Beta distribution is a

conjugate prior for the binomial likelihood.

This means that when the likelihood is binomial, which is the case for coin tosses, using a Beta prior results in a

posterior distribution that is also a Beta distribution.)

A 95% credible interval (CrI) is typically obtained by finding the 2.5th and 97.5th percentiles of the posterior

distribution. These percentiles can be computed using the inverse cumulative distribution function (CDF) for the

Beta distribution. For example,

\[

\begin{align*}

\text{CrI} &= [\text{invBeta}(0.025, 61, 41), \quad \text{invBeta}(0.975, 61, 41)]

&\approx [0.52, 0.68].

\end{align*}

\]

Given the observed data and the chosen prior, there is a 95% probability that \(p\) falls between 0.52 and 0.68.

This interval directly reflects our uncertainty about \(p\) after seeing the data.

You find the Bayesian credible interval "more intuitive" because it directly answers the question, “What is the probability

that the parameter falls within this interval given the data and our prior beliefs?” On the other hand, Frequentist methods

provide guarantees on long-run performance without the need for a prior, which can be an advantage in settings where subjective

beliefs are hard to justify.

Bootstrap

In situations where the estimator is a complex function of the data (for example, when it is not a simple maximum

likelihood estimator), or when the sample size is too small to reliably approximate its sampling distribution

analytically, we can use the bootstrap method.

This technique involves resampling the observed data with replacement to generate many "bootstrap samples," which are

then used to empirically estimate the sampling distribution of the estimator. This approach is especially useful when

traditional assumptions (e.g., normality) may not hold, providing a flexible, non-parametric way to assess uncertainty

and construct confidence intervals.

Example:

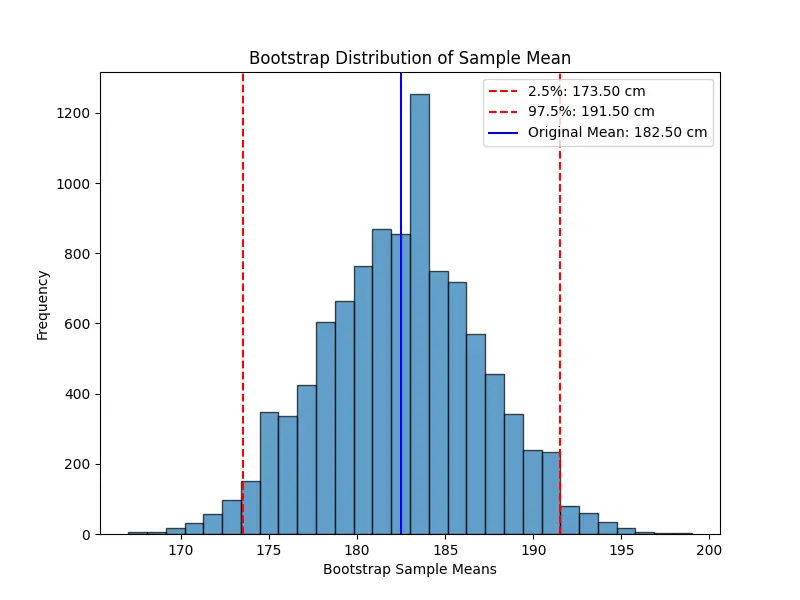

we have a small dataset of 10 people's heights (in cm):

\[

x = [160,165,170,175,180,185,190,195,200,205].

\]

The sample mean is \(\hat{\mu} = 182.5\). Since our sample size is small, we might not be able to assume the sampling

distribution of the mean is normal. Instead of relying on theoretical approximations, we use bootstrap resampling to

approximate it empirically.

Here, we randomly draw 10 values from the original sample with replacement. Some values may be repeated, and others may be

missing in a given resample. For example, we might obtain:

\[

\begin{align*}

&x_1 = [165,175,175,190,185,160,200,195,180,185], \\\\

&\hat{\mu} = 181.0.

\end{align*}

\]

Then we repeat this process many times (e.g., 10,000 times). Each time, we create a new resampled dataset, compute its mean,

and store it. Once we have 10,000 bootstrap sample means, we can use them to estimate the confidence interval: